Decoding Medicare Plan J Coverage: Your Guide to Supplemental Insurance

Are you feeling lost in the maze of Medicare options? Trying to figure out what supplements Original Medicare can feel like deciphering a secret code. This is especially true when you start exploring Medicare supplement plans, like Plan J. Let's shine some light on this option and break down what Medicare Plan J coverage entails, so you can navigate the world of supplemental insurance with confidence.

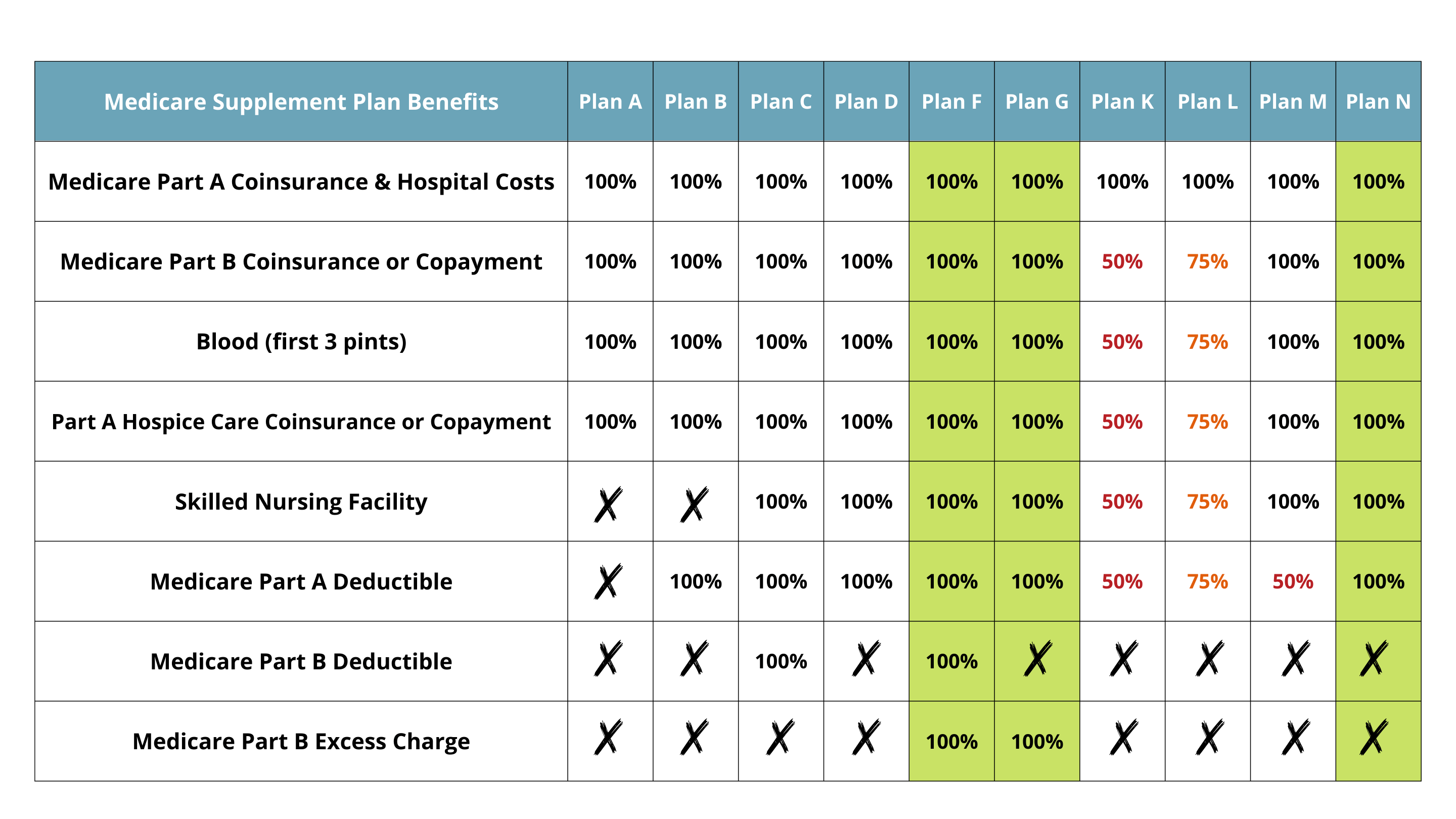

Medicare Plan J was a popular choice for supplementing Original Medicare (Parts A and B). It provided comprehensive coverage for many out-of-pocket expenses, giving beneficiaries peace of mind regarding their healthcare costs. Understanding the details of Plan J coverage is important, even though it's no longer available for new enrollees, as some individuals may still have this plan.

While Medicare Part A and Part B cover a substantial portion of healthcare costs, they don't cover everything. This is where Medicare Supplement, also known as Medigap, plans come in. These plans, like the former Plan J, are offered by private insurance companies and are designed to fill the "gaps" in Original Medicare coverage by helping pay for co-pays, coinsurance, and deductibles.

Medicare Plan J was designed to offer comprehensive coverage, covering 100% of the Medicare Part A deductible, coinsurance, and an additional 365 lifetime reserve days. It also covered the Part B deductible, coinsurance, and excess charges. This level of coverage meant that those with Medicare Plan J typically had predictable and manageable out-of-pocket healthcare costs.

Navigating the complexities of Medicare supplement plans is essential for anyone approaching retirement or currently enrolled in Medicare. Even though new beneficiaries can no longer enroll in Plan J, understanding its previous benefits and how it worked can help illustrate the importance of Medigap coverage and inform decisions about choosing a different plan that best fits one's needs today.

Medicare Supplement Plan J was established as part of the standardized Medigap plans offered by private insurance companies. These plans were created to help beneficiaries manage the out-of-pocket costs associated with Original Medicare.

One of the key benefits of Medicare Supplement Plan J was its comprehensive coverage, reducing financial stress related to healthcare expenses. For example, Plan J covered the Part A deductible, which could be a significant amount. It also covered Part B excess charges, which are the difference between what a doctor charges and what Medicare approves. This protection offered peace of mind to those concerned about unexpected medical bills. However, it's important to note that Plan J, like other Medigap plans, does not cover prescription drugs. Medicare Part D or a Medicare Advantage plan with drug coverage is needed for prescription drug coverage.

Beneficiaries who already have Plan J can generally keep their coverage. While they can switch to another Medigap plan, it's important to understand the rules and potential costs associated with switching. Those new to Medicare should explore the available Medigap plans and compare benefits and premiums to choose the best option for their needs.

Advantages and Disadvantages of Medicare Plan J

| Advantages | Disadvantages |

|---|---|

| Comprehensive coverage of many out-of-pocket costs | No longer available for new enrollment |

| Predictable healthcare expenses | Potentially higher premiums than other Medigap plans |

Frequently Asked Questions about Medicare Plan J:

1. Can I still enroll in Medicare Plan J? No, Plan J is no longer available for new enrollees.

2. What are the alternatives to Medicare Plan J? Other Medigap plans, such as Plan G, Plan N, and high-deductible Plan G are available.

3. Does Medicare Plan J cover prescription drugs? No, it does not. You would need a Part D plan or a Medicare Advantage plan with prescription drug coverage.

4. How do I find out more about current Medigap plans? You can contact your State Health Insurance Assistance Program (SHIP) or visit the Medicare.gov website.

5. Can I change my Medigap plan if I have Plan J? Yes, you can switch to another Medigap plan, but understand the rules and potential underwriting requirements.

6. What factors should I consider when choosing a Medigap plan? Consider your budget, health needs, and the coverage offered by different plans.

7. Are there any resources that can help me compare Medigap plans? Yes, the Medicare.gov website provides tools to compare Medigap plans in your area.

8. How do I find out if my doctor accepts Medicare assignment? You can contact your doctor's office or check the Medicare.gov Physician Compare tool.

Tips and tricks for those with Medicare Plan J: Keep your policy information updated and review your coverage annually to ensure it still meets your needs.

In conclusion, Medicare Plan J, while no longer available for new enrollees, served as a valuable supplement to Original Medicare, offering comprehensive coverage and predictable healthcare costs. While Plan J itself is no longer an option, understanding its benefits and how it worked highlights the importance of exploring available Medigap plans. For those new to Medicare, exploring the current options like Plan G, Plan N, and high-deductible Plan G is crucial. Choosing the right Medigap plan allows you to manage out-of-pocket expenses and provides financial security in the face of healthcare costs. Take the time to research your options, compare plans, and select the coverage that best aligns with your health needs and budget. Reach out to your State Health Insurance Assistance Program (SHIP) for personalized guidance. Making informed decisions about your Medicare coverage empowers you to navigate the healthcare system confidently and enjoy the benefits of comprehensive coverage throughout your retirement.

Engaging spanish activities for 3rd grade fun learning

Unraveling the complexities of wiring harness types

Unlocking mlb predictions your guide to espn expert picks