Navigating Medicare Gaps AARP Plan F Supplemental Insurance

Are you grappling with the complexities of Medicare and wondering how to ensure comprehensive coverage? Medicare, while essential, doesn't cover all healthcare expenses, leaving potential gaps in your financial protection. This is where supplemental insurance, like AARP Plan F (prior to 2020), steps in. This article will explore AARP's role in offering Medigap Plan F and discuss options available to those who aged into Medicare before 2020 and maintain their existing Plan F coverage.

AARP, a prominent advocacy organization for individuals over 50, doesn't directly underwrite insurance. Instead, they endorse plans offered by UnitedHealthcare Insurance Company. Understanding this distinction is crucial when navigating the supplemental insurance landscape. If you currently hold AARP-endorsed Plan F coverage, it's essential to be aware of its provisions and how it complements your existing Medicare benefits.

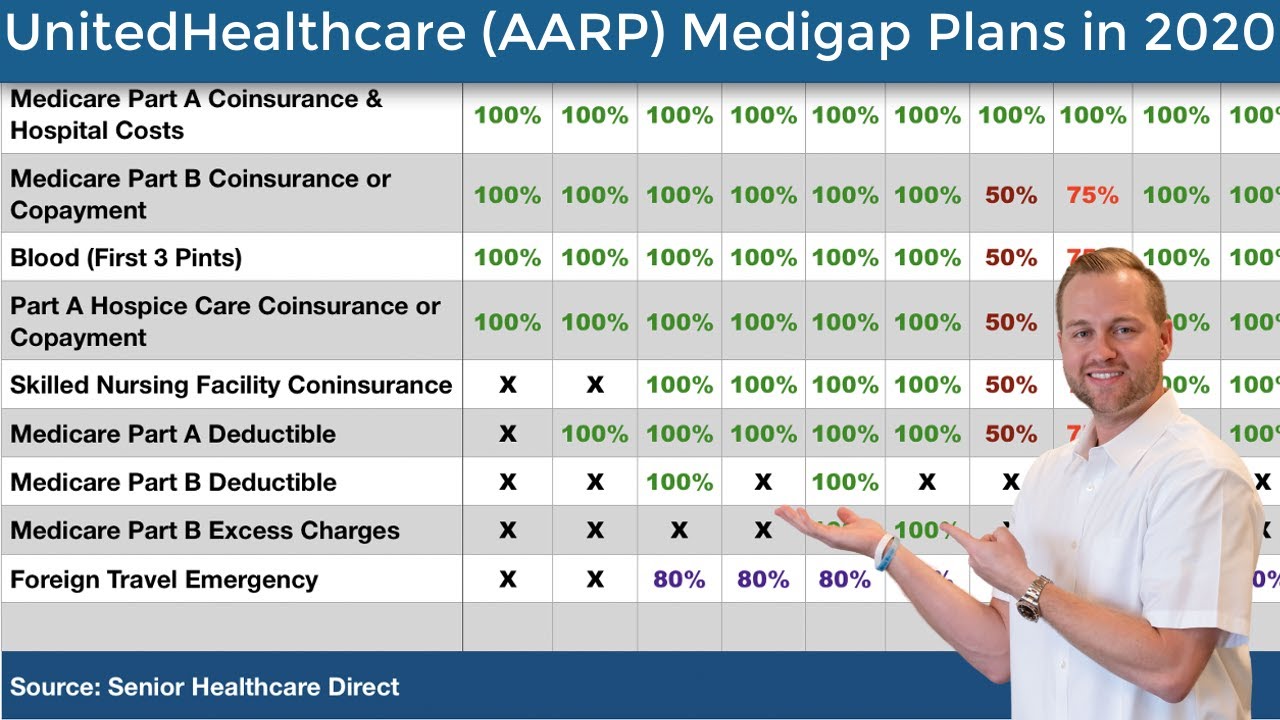

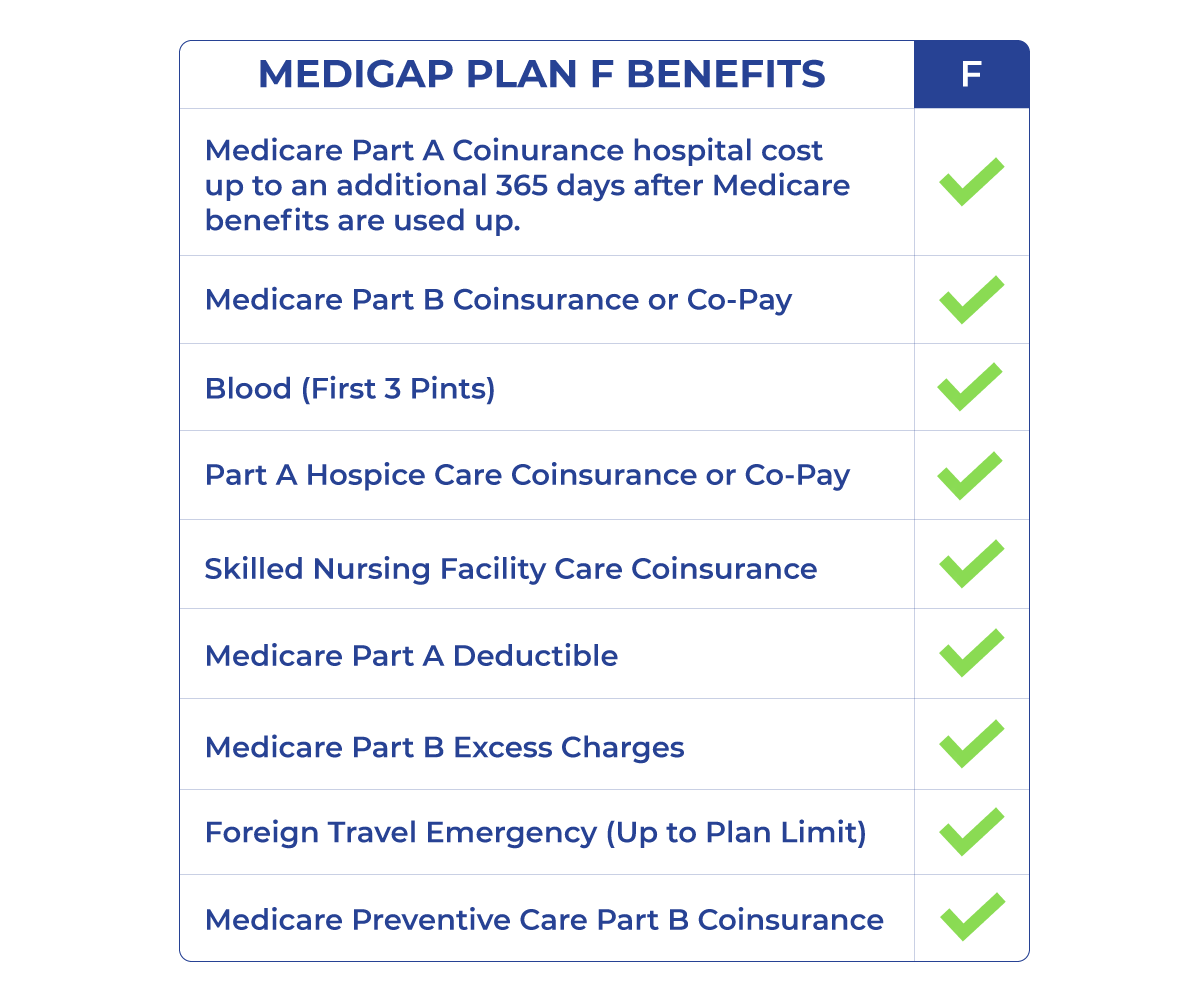

Before 2020, AARP Plan F provided comprehensive coverage for Medicare's cost-sharing, including deductibles, coinsurance, and copayments. This provided a significant financial safety net for beneficiaries. However, changes in Medicare regulations impacting plans available to new Medicare beneficiaries after January 1, 2020, mean Plan F is no longer available to those newly eligible for Medicare. This is due to the plan covering the Part B deductible, which Congress decided could incentivize overuse of healthcare services.

Navigating the Medicare system can feel overwhelming. Understanding the nuances of supplemental coverage, especially if you're considering or currently enrolled in AARP Plan F, requires careful consideration. This article aims to empower you with the information needed to make informed decisions about your healthcare coverage.

Let's delve into the specifics of AARP Plan F, including its historical context, coverage details, and relevant alternatives for those not eligible for this plan. By exploring these aspects, we can clarify the role of supplemental insurance in maximizing your Medicare benefits.

The history of Medigap plans like Plan F is tied to the development of Medicare itself. As gaps in Medicare coverage became apparent, private insurers stepped in to offer supplemental policies. AARP's endorsement of UnitedHealthcare's Plan F became a popular choice due to its comprehensive coverage. This partnership highlighted the importance of filling Medicare's gaps to avoid unexpected medical expenses.

For those who aged into Medicare before 2020 and still have AARP Plan F, it means your plan continues to cover Medicare-approved charges that Original Medicare doesn't, like the Part A deductible, Part B deductible (no longer covered by plans available to new Medicare beneficiaries), coinsurance, and copayments. This predictability is highly valued by many beneficiaries.

If you're considering switching from Plan F, carefully compare the coverage and costs of other Medigap plans. Plans like Plan G and Plan N offer similar coverage but may have different out-of-pocket costs. Consult with a licensed insurance agent or use online comparison tools to understand your options fully.

Advantages and Disadvantages of AARP/UnitedHealthcare Plan F

| Advantages | Disadvantages |

|---|---|

| Predictable out-of-pocket expenses (for those who maintain existing coverage). | No longer available to new Medicare beneficiaries. |

| Comprehensive coverage for most Medicare cost-sharing (for those who maintain existing coverage). | Can be more expensive than other Medigap plans. |

Frequently Asked Questions

1. Is AARP Plan F still available? No, not to new Medicare beneficiaries.

2. What are alternatives to AARP Plan F? Plans G and N offer similar coverage.

3. Does AARP offer other Medigap plans? Yes, through their endorsement of UnitedHealthcare, other Medigap plans are available.

4. How can I enroll in a Medigap plan? Contact a licensed insurance agent or visit Medicare.gov.

5. When can I enroll in a Medigap plan? The best time is during your Medigap Open Enrollment Period.

6. What is the Medigap Open Enrollment Period? It's a six-month period that starts when you're both 65 or older and enrolled in Medicare Part B.

7. How much does AARP Plan F cost? Premiums vary based on location and other factors.

8. Can I be denied coverage for a Medigap plan? During the Medigap Open Enrollment Period, you generally cannot be denied coverage or charged higher premiums based on pre-existing conditions.

In conclusion, while AARP Plan F is no longer an option for those newly eligible for Medicare, those who aged into Medicare before 2020 and maintain their Plan F coverage can continue to benefit from its comprehensive coverage. Understanding the details of your AARP/UnitedHealthcare Medigap Plan F or exploring alternative Medigap plans is crucial for making informed decisions about your healthcare future. Consult with a licensed insurance agent or utilize online resources to compare plans, evaluate your individual needs, and choose the best coverage for your situation. Don't hesitate to proactively manage your healthcare costs and secure the peace of mind you deserve.

The subtle art of bowling ball care with simple green

Unlock serenity with benjamin moores sand dunes your guide to coastal calm

Decoding sherwin williams paint disposal a guide to eco friendly practices