Navigating Medicare Supplement Plan E: Comprehensive Coverage Guide

Are you feeling overwhelmed by the complexities of Medicare? Choosing the right supplemental coverage can feel like navigating a maze. This comprehensive guide will shed light on Medicare Supplement Plan E, a popular choice for those seeking robust protection against out-of-pocket healthcare costs. We'll explore the ins and outs of Plan E coverage, helping you determine if it's the right fit for your needs.

Medicare can be a valuable safety net, but it doesn't cover everything. That's where Medicare Supplement (Medigap) plans come in. These plans, offered by private insurance companies, help fill the gaps in Original Medicare coverage, leaving you with fewer unexpected expenses. Plan E is one such option, offering specific benefits tailored to address common healthcare costs.

Understanding the nuances of Medicare Supplement Plan E coverage is crucial for making informed decisions about your healthcare. This guide will equip you with the knowledge you need to confidently navigate the Medicare landscape. We'll delve into the specifics of Plan E, comparing it to other Medigap options and highlighting its key advantages and disadvantages. By the end, you'll have a clear understanding of how Plan E can help you manage your healthcare budget.

Navigating the Medicare system can be challenging, but it doesn't have to be. This guide will provide you with practical tips and actionable steps for selecting the right Medigap plan. We'll address common questions and concerns, providing you with the resources you need to make confident choices about your healthcare coverage.

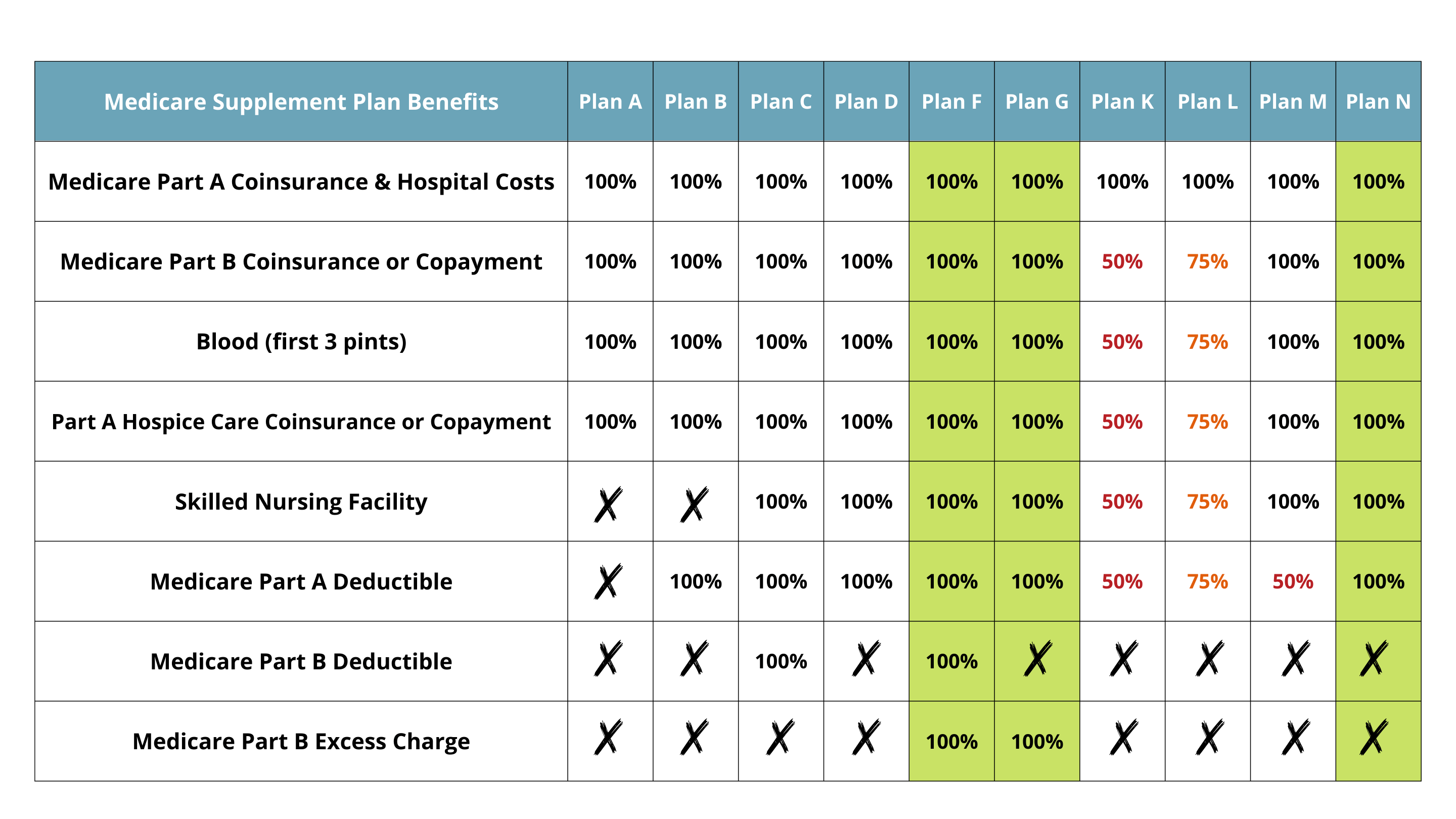

Medicare Supplement Plan E offers comprehensive coverage for many of the out-of-pocket expenses not covered by Original Medicare. These include Part A hospital coinsurance, Part B coinsurance or copayment, the first three pints of blood used in a medical procedure, and skilled nursing facility coinsurance. This comprehensive coverage offers peace of mind, knowing that you are protected from many potential healthcare costs.

Medicare Supplement plans were standardized in 1992, creating a system where plans with the same letter offer the same benefits regardless of the insurance provider. Plan E became a popular option because of its broad coverage. However, changes to Medicare and the introduction of Plan F and Plan G have shifted the landscape. While Plan E is no longer offered to new Medicare beneficiaries, understanding its features can still be valuable for those currently enrolled.

One of the biggest challenges with Medicare Supplement plans in the past was varying coverage from different insurers. Standardization solved this issue, ensuring consistency across all Plan E offerings. This consistency simplifies comparison shopping and ensures predictable benefits.

Plan E covers 100% of Part A hospital coinsurance after Medicare benefits are exhausted, 100% of Part B coinsurance or copayment, the first three pints of blood, and 100% of the Part A skilled nursing facility coinsurance. One example is if a patient requires a blood transfusion and uses three pints, Plan E would cover the cost of those pints. Another example is covering the costs associated with an extended hospital stay beyond the time covered by Medicare Part A.

Advantages and Disadvantages of Medicare Supplement Plan E

| Advantages | Disadvantages |

|---|---|

| Comprehensive coverage for hospital and medical expenses. | No longer available to new Medicare beneficiaries. |

| Predictable out-of-pocket costs. | May have higher premiums than some other plans. |

While Plan E is no longer available to new Medicare beneficiaries, those currently enrolled can continue their coverage. It's important to understand your options and to periodically review your plan to ensure it still meets your needs. Consulting with a licensed insurance broker specializing in Medicare can be a valuable resource.

Here are some frequently asked questions about Medicare Supplement Plan E:

1. What does Medicare Supplement Plan E cover? Answer: Part A hospital coinsurance, Part B coinsurance or copayment, the first three pints of blood, and skilled nursing facility coinsurance.

2. Is Plan E still available? Answer: Not to new Medicare beneficiaries.

3. What are the alternatives to Plan E? Answer: Plan G and Plan N are popular alternatives.

4. How do I find a Medicare Supplement Plan E provider? Answer: Consult with a licensed insurance broker specializing in Medicare.

5. What is the cost of Medicare Supplement Plan E? Answer: Premiums vary by location and insurance company.

6. Can I switch from Plan E to another plan? Answer: Yes, you can switch plans during the Medicare Open Enrollment period or under certain circumstances.

7. What are the benefits of having a Medicare Supplement plan? Answer: Predictable out-of-pocket costs and peace of mind.

8. How do I learn more about Medicare Supplement plans? Answer: Contact your State Health Insurance Assistance Program (SHIP).

Choosing the right healthcare coverage is crucial for your financial well-being and peace of mind. While Medicare Supplement Plan E is no longer available for new enrollees, understanding its features and benefits can provide valuable context for navigating the Medicare landscape. This guide has provided a comprehensive overview of Plan E, including its coverage, advantages, disadvantages, and frequently asked questions. If you are currently enrolled in Plan E, it's essential to stay informed about changes to Medicare and to periodically review your coverage to ensure it still meets your evolving needs. If you're new to Medicare, explore the available Medigap options, such as Plan G or Plan N, to find the best fit for your individual circumstances. By taking the time to thoroughly research and compare plans, you can make informed decisions that empower you to manage your healthcare costs effectively and enjoy greater peace of mind.

Mental health resources in springfield ma baystate health psychiatry

Unleash the power of titanium wheel lug nuts lighter stronger faster

Unlocking the secrets of behrs most enviable greige paint